Energy Market Happenings

Energy Market Happenings

Energy markets continue to have bullish sentiment, despite oil markets being dragged down this week on renewed pandemic fears as lockdowns in Asia put a short-term halt on oils’ $70 dollar price handle. However, global oil supply remains in deficit despite the isolated new lockdowns, as many raw materials remain in high demand.

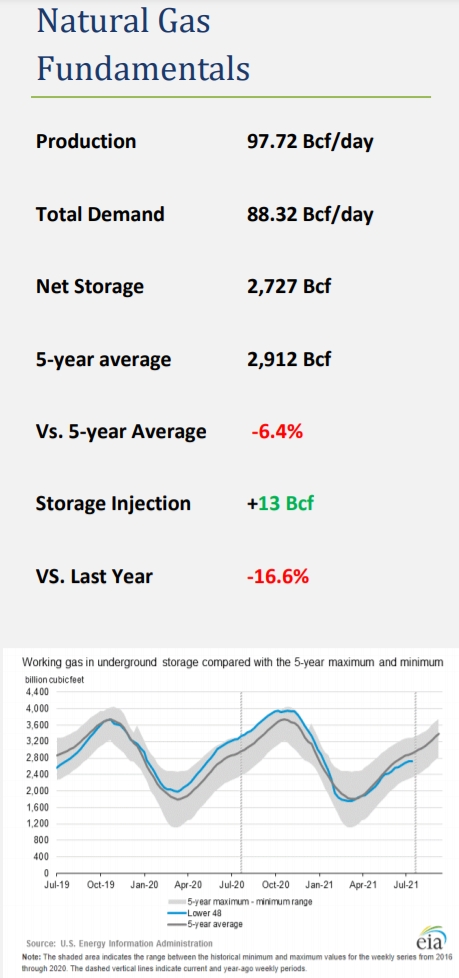

U.S. electricity and natural gas markets continue their bull run as all major trading hubs are up week-over-week due to rather bullish short-term weather forecasts. Mideast tensions and favorable US job data are also putting upward pressure on the energy sector. As we move through the summer peak demand levels, fuel sources like natural gas will have an opportunity to replenish stocks before winter withdrawal season beings. As it stands, natural gas markets are pricing in the winter risk and an end-ofwinter storage level of 1.5 TCF.

In the week ahead, we expect energy markets to start signaling major tops, also known as overbought conditions, and begin to sell-off as more forecasts and hurricane information is available.

As such, we initiated a short natural gas position on Friday via the ETF KOLD @ $15.84 with a target of $16.94, settling today @ $16.88.

Electricity

Electricity prices in western US highlight the price action on the power side as the past two months have seen record temperatures, drought, and wild-fires – depleting hydro-generation and causing transmission outages. This has resulted in a $20/mWh increase in day ahead prices

over the same period and withdrawal of natural gas from central plains storage as many western generators were forced to switch from hydropower to natural gasfired power generation.

ERCOT (Texas) saw spot prices retreat while forward markets have followed the major hubs, up across all calendar year strips in 2022 and beyond. This market is heavily backwardated with the further out calendar year strips trading at steep discounts to the near term.

East markets were also elevated weekover-week with all PJM and MISO hubs settling to the upside. Near-term strips continue to decouple from further out calendar years, with as much as a 13% difference in price.

We see natural gas prices gravitating back toward $4 dollars/MMBtu and could easily fall back toward $3.85 if weather normalizes out west and demand begins its decent toward fall levels

Natural Gas

Natural gas consumption is set to peak this month which will help put bearish pressure on spot prices after a week in which the prompt month contract rose $.23/MMBtu primarily driven by the current 10–15-day forecast. At the same time pipeline nominations are holding dry natural gas production above 92/Bcf day. With wind generation and LNG feed gas flows flat this week, the overall net impact to

natural gas storage is neutral.

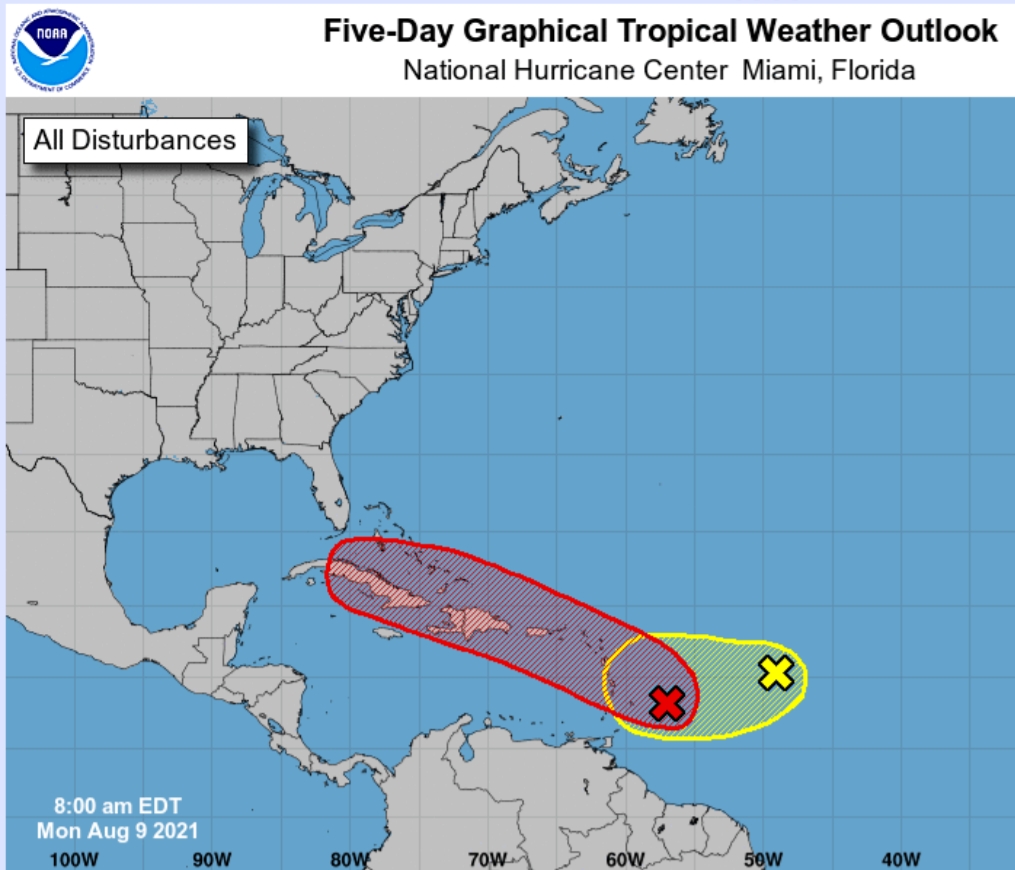

This week we expect a natural gas storage injection of +60 for the weeking ending August 6 compared to the five year average +44bcf. Additionally, market participants will be keeping a close eye on the two tropical distrubances that have a 70% chance of forming a named Hurricane. Hurricanes disrupt both supply and demand.

In the long term, foreign natural gas trading hubs are more than $16MMbtu for spot September pricing, this is the highest level since 2013 (Platts). This is bullish for liquified natural gas (LNG) which is down this past week and may see some interruptions due to hurricanes, but the long-term fundamentals support a sector of growth. In Asian, hot weather has their power burn (electricity generated by natural gas) up heavily y-o-y which should also lead to continued demand for US LNG.

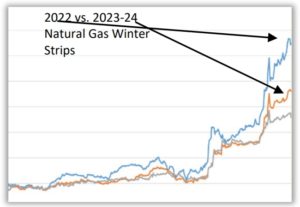

Winter Strips

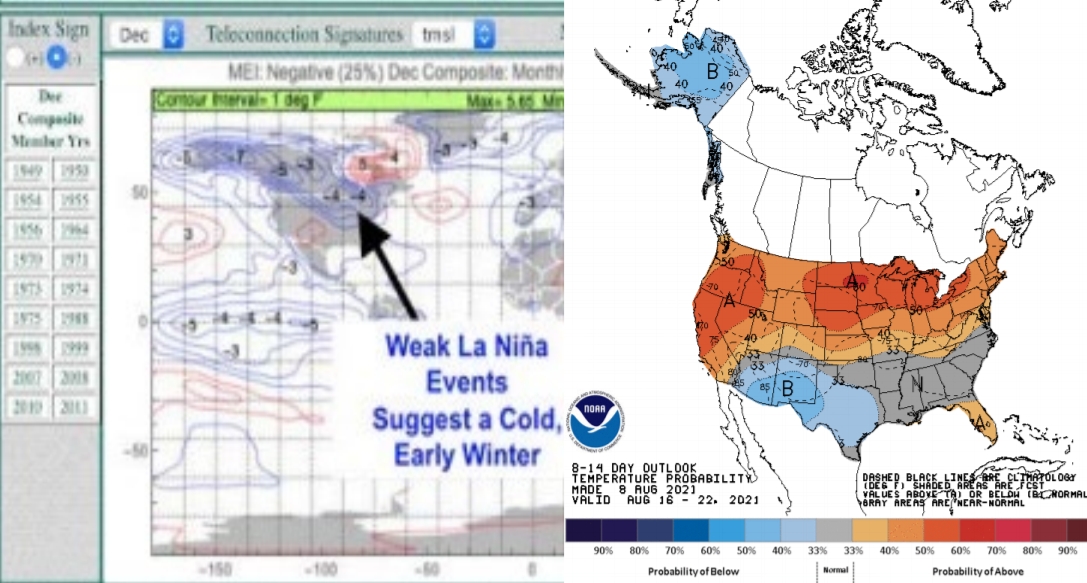

Over the past two months, 2022 calendar strips and winter strips

have decoupled from 2023-24. This spread is likely to continue

through the winter if we see even a weak La Nina – which brings

colder than normal temps to major energy consumption trading

hubs across the US.

Weather Focus

Short-term weather remains above normal for most of the country, a bullish price signal for natural gas and electricity during the summer; however, longer range models are right in line with the 30-year average, and if the long-range forecast holds true, expect more downside price action for natural gas markets especially.

Two active tropical depressions are being tracked through the Atlantic, but it is too early to tell if they will impact production, LNG exports, and domestic demand.

Major events to keep an eye on this week will be the tropical disturbances in the Atlantic and the strength of a potential La Nina formation along the Pacific equator. Cooler water surface temperatures lead to a LA Nina formation which suggests a cold and early winter for the northern half of the US.

Disclaimer: Taurus Advisory Group believes all information described herein to be reliable and does not represent or warrant as to its accuracy. All representations and estimates included herein were prepared solely for informational purposes only and is not advice regarding the value of trading in commodity markets as defined in the Commodity Exchange Act. Taurus Advisory Group does not make and expressly disclaims, any express or implied guaranty, representation or warranty regarding any opinions or statements set forth herein. Taurus Advisory Group shall not be responsible for information contained herein or for any omission or error of fact that may be discovered. This material shall not be reproduced (in whole or in part) to any other person without the prior written approval of Taurus Advisory Group.