Yesterday, the 2020-23 calendar year strips for natural gas contracts hit their all-time lows, trading at $2.647, $2.667, $2.716, and $2.784, respectively. Meanwhile, the near-term prices for the prompt month contract (June) and the twelve-month strip (June-May19) remain range-bound, trading off end-of-summer natural gas storage projections and summer weather forecasts. The forward strips are suppressed mainly due to impressive natural gas and oil production numbers that have eased any fears of future supply shortages and equally impressive equity market growth. While new steel and aluminum tariffs may impact the marginal return of new oil and gas producers, there is enough growth and increases in efficiency for producers to remain economically viable and, therefore, keep downward pressure on forward prices.

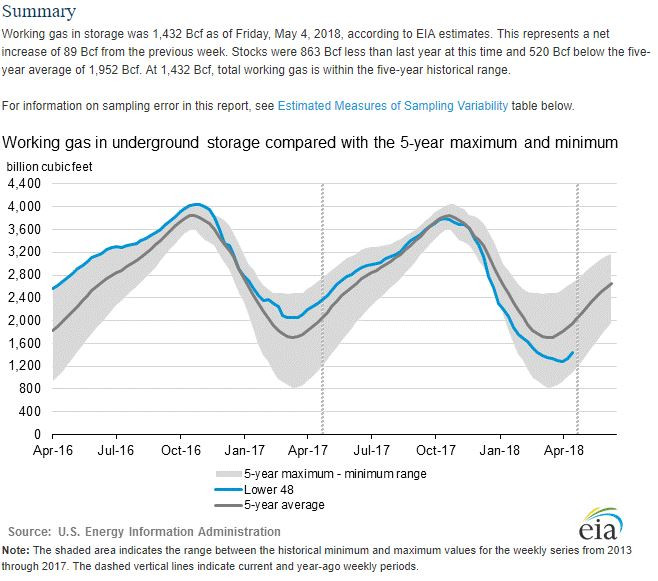

After settling lower yesterday, every single month through April 2020 increased this morning after the EIA released its weekly natural gas storage number. The EIA reported an injection of +89 Bcf compared to +45 Bcf last year and +75 Bcf for the five-year average. Inventories now stand at 1,432 Bcf, a deficit of 37.6% to last year and 26.6% to the five-year average. A higher storage number vs. last year and the five-year average did not inspire a sell-off as expectations were higher than +89 Bcf and above-normal weather is forecasted to limit triple digit injections in the coming weeks.

Despite today’s rally, most traders have decreased their long positions (bets that prices will rise) as record natural gas production has kept the market in balance. That balance is tightening after the coldest April since 1983 and the fifth coldest since 1950 unexpectedly reduced natural gas storage until its first injection last week.This balance will continue to tighten and be supportive of prices if cooling degree days increase faster than expected, which is the current forecast for the mid-May to early-June. If production can hold off the increases in demand, then we should be in line with last year’s end-of-summer storage – a likely bearish scenario for the Fall shoulder season.

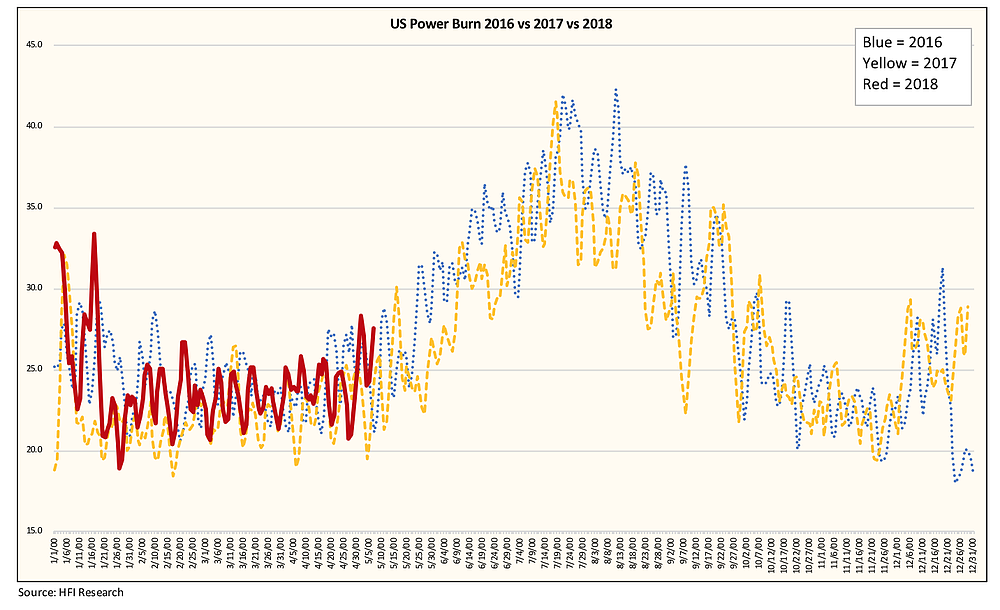

Other fundamentals that have made an impact early in 2018 are power burn (natural gas used to generate electricity), inflation, equity markets, and commodity exports to Mexico and China. Power Burn is up y-o-y as depicted below, Liquified Natural Gas (LNG) is setting export records daily with robust demand overseas, and the strength of the dollar, which hit its all-time low earlier this year before a recent plateau, will remain key indicators for natural gas and electricity prices this year.