Despite lingering cold weather and historic natural gas storage deficits, the market continues to view the ramp up in production as sufficient expected supply for the coming winter.

With storage projected to rebound over the summer leaving 2018-19 winter with an estimated 3.8 tcf of gas, market participants are anxiously awaiting updates on the summer weather forecasts. A well-above normal summer scenario will drive futures into a rally as increased power burn (natural gas used for power generation) will diminish end of summer storage levels (The EIA is predicting a 2% increase in power burn this summer). A mild summer will allow for natural storage levels to strengthen, leaving little room for the bulls to push the market higher. Until summer demand and weather forecasts become more certain, both power and gas markets are expected to remain range bound over the summer with little volatility despite the profound tightness in storage deficits. Other opinions seem to think the lack of buying interest in the summer strips is an indication that volatility will return and in a very dramatic way. As one outlet put it, ‘Make Volatility Great Again’ which could be the case if an early heat-wave arrives.

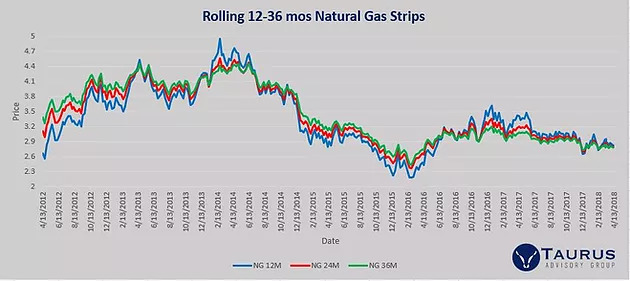

After two dips in December and February, the 12-36mos forward natural gas strips have settled in around the $2.80 level and we are expecting prices to remain in the range of $2.56-$3.00/Mmbtu throughout the summer.

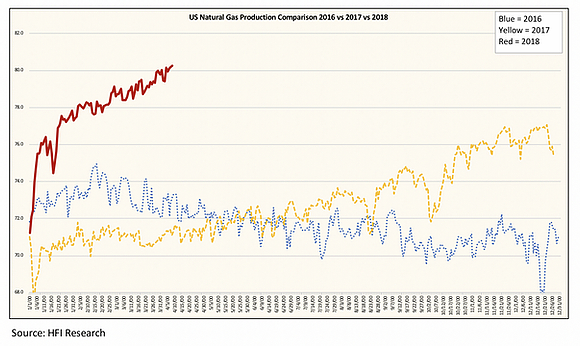

The Energy Information Administration published their Short-Term Energy Outlook this week and it reinforces forecasts that natural gas production to average 81.1 Bcf/d in 2018, a new record. Additionally, they expect supplies to increase by another 1.7 Bcf/d in 2019. This is another indication that the marginal return for producers is much lower than many speculate. Larger producers will continue to allow supply to increase which should inspire downward pressure on prices and reduce profits. If smaller producers cannot maintain profitability at lower prices, consolidation will ensue, and larger producers will gain market share and drive prices back up. The global oil markets over the past two years are a great example of this as oil prices dropped from over 100 dollars/barrel to as low as 28 dollars/barrel and then rallied to above 60 dollars early this year. The profitability of producers should not be dismissed as a price manipulator, but remains just one piece of the speculation puzzle.

Updated Natural Gas production comparison vs. 2017 and 2018 from HFI Research: